For public-funds investors, mid-year is often when planning assumptions begin to meet operational reality. Cash balances may remain elevated longer than expected. Project timelines may shift. Reserve use may become more immediate, or less immediate, than originally assumed. Even when those changes seem operational rather than investment-related, they can materially affect whether a portfolio is still positioned the way it should be.

High-performing municipal investors do not treat mid-year as a passive checkpoint. They use it to ask whether the portfolio still fits the entity it serves. Seen that way, strong performance is not only about return. It is also about alignment, discipline, and timely reassessment.

What makes a checkup useful is not a date on the calendar but the distance from the start of the year. Fiscal years differ across public entities, and the value of stepping back comes less from a precise moment than from enough time having passed for the year’s opening assumptions to be tested against how conditions have actually developed.

When Assumptions Change, Portfolio Decisions Can Change With Them

At the beginning of a fiscal year, portfolio decisions are often made against a reasonable set of expectations. But by mid-year, those expectations may have shifted in meaningful ways. An entity may be carrying more liquidity than anticipated, working through delayed capital spending, or holding reserve balances that are still unlikely to be used in the near term. In other cases, operating demands may be arriving sooner than expected.

Those changes do not automatically mean a portfolio should be restructured. But they do mean the portfolio should be reviewed with current information rather than left aligned to assumptions that may no longer be accurate.

What Portfolio Health Means at Mid-Year

A mid-year review is not just a performance check. It is a broader reassessment of portfolio health. And portfolio health is not simply a measure of earnings; it is a measure of fit. A healthy portfolio should still reflect the entity’s liquidity needs, balance purpose, policy constraints, concentration comfort, and operating reality.

That distinction matters because a portfolio can look stable on the surface while quietly drifting out of alignment underneath. Returns may still appear acceptable even as the assumptions beneath the structure go stale. The strongest reviews look past what a portfolio earned and ask whether it still matches the entity it serves.

A Practical Mid-Year Review Framework

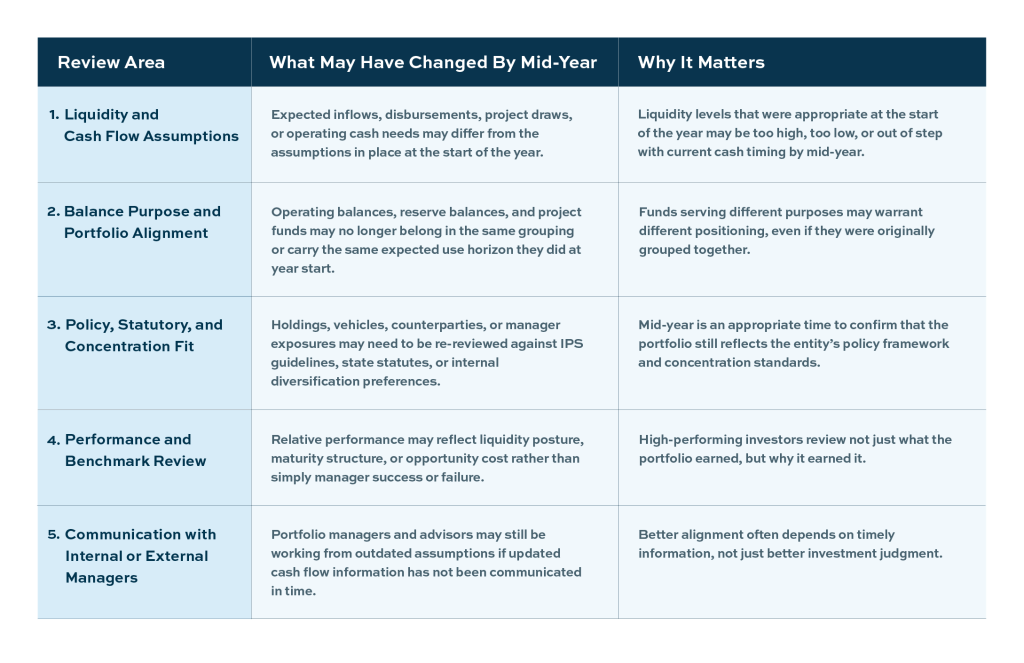

Some of the most effective mid-year reviews focus on five areas that directly affect portfolio alignment, liquidity readiness, and overall stewardship. The goal is not to create unnecessary activity. It is to confirm that the portfolio still reflects the conditions it was built to serve.

In practice, this is where disciplined programs can separate themselves. They do not simply note that conditions have changed; they weigh whether the change is large enough to affect liquidity posture, portfolio alignment, or the opportunity set available within policy.

Consider a public entity that entered the year expecting a large capital draw over the summer and kept a meaningful balance on the front end of the curve. By mid-year, the project timeline had slipped and the draw was now expected much later. If the shift was only a few weeks, the original positioning might still be appropriate. But if the balance was unlikely to be needed for another year, a mid-year review is where that structure gets revisited. In a more normal curve, where shorter liquidity vehicles may yield less than longer maturities, leaving those funds positioned for an outdated near-term need can cost both earnings and alignment.

Why Communication Is Part of Portfolio Health

Communication is one of the most overlooked parts of mid-year oversight. Better outcomes are not driven only by market conditions or portfolio construction, but by how quickly and accurately new operating information reaches the investment process.

When internal teams and external advisors are working from the same current assumptions, the portfolio is more likely to remain aligned with actual needs. When cash flow changes, project delays, reserve-use updates, or spending shifts are communicated late, portfolio decisions may continue to reflect outdated information. In that sense, portfolio health is partly an investment question and partly an information-flow question.

What the Mid-Year Review Should Accomplish

Mid-year portfolio checkups are not about unnecessary trading or change for its own sake. They are about confirming that the portfolio still fits the entity behind it: its liquidity needs, the purpose of each balance, its policy constraints, and its operating reality.

Strong oversight means revisiting assumptions before they quietly go out of date. Typically, the best mid-year reviews do not stop at whether the portfolio performed as expected. They ask whether it still fits the job it is there to do.

About Deep Blue Investment Advisors

At Deep Blue Investment Advisors, we specialize in helping government finance officers expand their horizons by diving into fixed-income management solutions with tangible results. Our team of experienced investment management professionals can help tailor a portfolio to your investment needs while providing regular reporting, portfolio compliance, and performance meetings. You can always count on us to prioritize our relationships, provide guidance, and act in your best interest.

To speak with an advisor or for additional information about this article or Deep Blue Investment Advisors, please connect with one of our advisors today.

Deep Blue Investment Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. This communication is provided for informational purposes only and is not an offer to sell or a solicitation of an offer to buy any investments offered by Deep Blue Investment Advisors, nor shall any such investments be offered or sold to any person in any jurisdiction in which such an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Past performance is not an indicator of future results.

The information set forth herein is intended only for the person or entity to which it is addressed. By accepting this communication, you agree to maintain the confidentiality of its contents and agree not to distribute this communication to any other person or to use it other than for the purposes described above.