When revenue feels uncertain, the instinct is to wait.

Across many public entities, federal funding has become a more unpredictable piece of the overall revenue picture. Timing is less certain, policy direction is less clear, and assumptions that held a year ago are being revisited. In that kind of environment, holding reserves in overnight accounts can feel like the safest possible move.

It is also a decision with consequences.

When “Waiting” Becomes a Strategy

Idle reserves are rarely framed as an active choice, but in periods of uncertainty, they often become one. The logic is straightforward: if funding timing is unclear, liquidity should be maximized.

That thinking is directionally correct, but it can be taken too far.

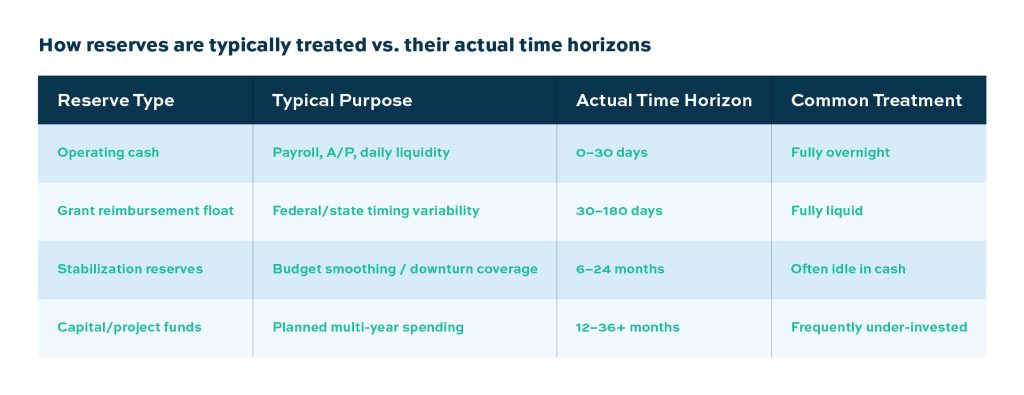

Not all reserves are equally exposed to federal timing risk. Some funds are tied directly to near-term obligations or reimbursement cycles. Others sit further in the background, supporting longer-term stability or acting as contingency buffers. Treating all reserves as if they are needed tomorrow can lead to an overly conservative posture that leaves meaningful income on the table.

Separating Timing Risk from Liquidity Needs

A more durable approach is to separate what is uncertain from what is unknown.

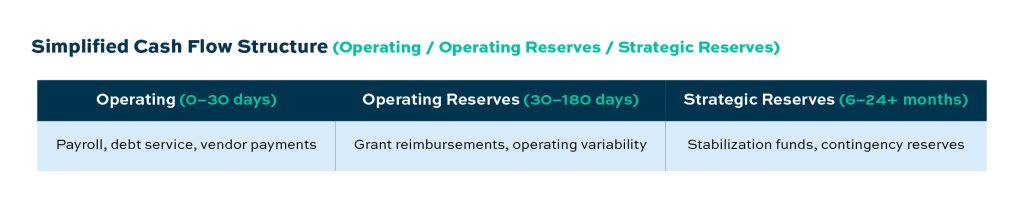

Federal funding may introduce variability in timing, but it does not typically eliminate visibility into baseline operating needs. Payroll, debt service, and core expenditures still follow relatively predictable schedules. That foundation creates an opportunity to segment reserves more precisely.

Funds that may be needed on short notice should generally remain in highly liquid, stable structures. But funds that are less sensitive to federal timing, even in an uncertain environment, can be evaluated for modest extension along the yield curve.

This is not about reaching for yield. It is about recognizing that uncertainty is not uniform across all dollars.

The Cost of Over-Conservatism

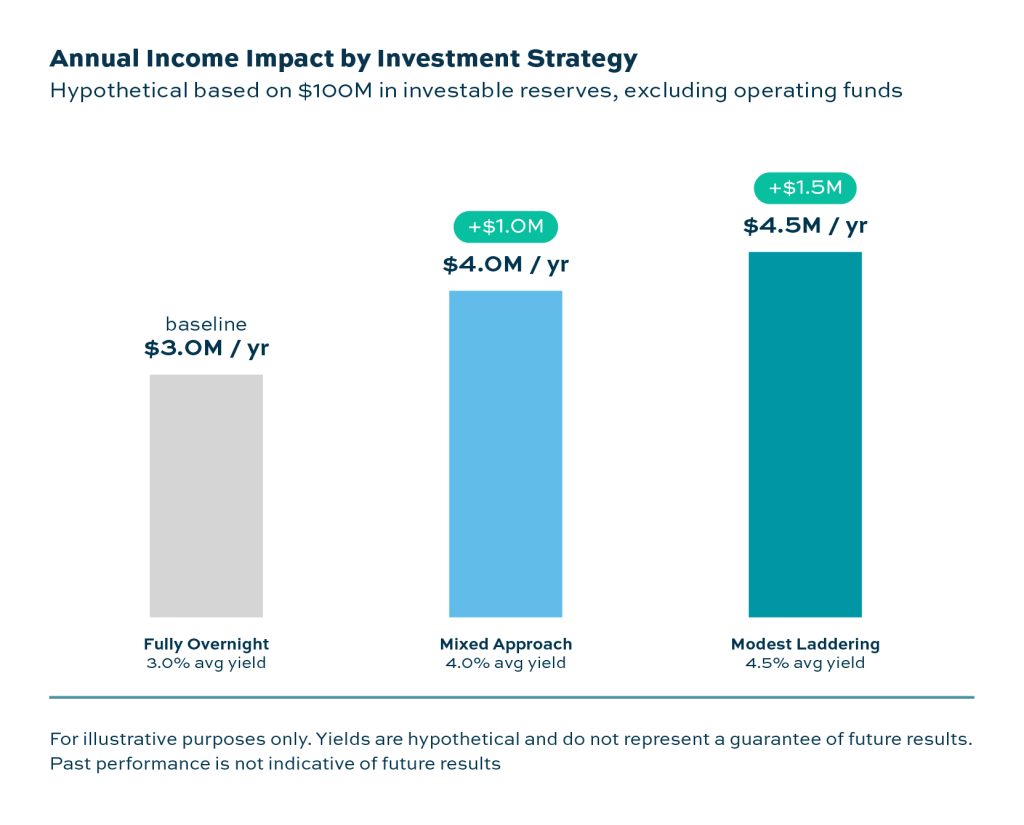

In a declining or unstable rate environment, the cost of holding excess cash in overnight accounts becomes more visible. As rates move, income adjusts immediately, often downward, with no offset.

For entities managing large reserve balances, even small differences in yield can translate into meaningful changes in annual interest income. When those reserves are left entirely uninvested beyond overnight structures, the opportunity cost compounds quietly in the background.

That trade-off may be appropriate for a portion of funds. It is rarely appropriate for all of them.

Hypothetical Illustration: Annual income impact (assuming $100M in investable reserves, excluding operating funds)

The illustration below compares three investment approaches applied to the same pool of investable reserves ($100M, excluding operating funds). Each strategy represents a different posture — from keeping all reserves in overnight accounts to extending maturities along a modest ladder. The difference in annual income shown reflects how yield changes based on how reserves are structured. The goal is not to maximize return at the expense of liquidity, but to illustrate the opportunity cost of leaving all reserves idle when only a portion genuinely needs to be.

A Measured Path Forward

The objective in uncertain periods is not to predict outcomes. It is to build a structure that can accommodate a range of them.

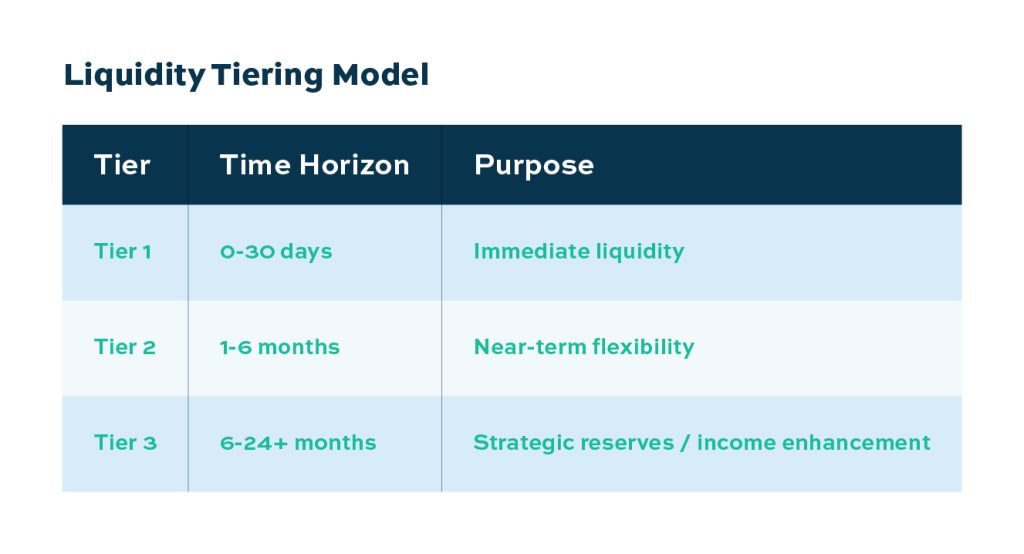

A modest laddering approach, applied to a portion of reserve balances, can help balance liquidity and income. Staggered maturities provide periodic access to cash while reducing reliance on a single rate environment. At the same time, maintaining a clearly defined liquidity tier helps ensure that near-term needs are not compromised.

The result is not a dramatic shift in strategy, but a more intentional one.

The Takeaway for 2026

Uncertainty does not eliminate the need to make decisions. It changes how those decisions should be made.

If there is one idea worth carrying forward, it is this: not all reserves should be managed as if they are immediately at risk. Some require maximum flexibility. Others can be positioned to remain productive, even while the broader funding picture remains in flux.

The discipline lies in knowing the difference.

About Deep Blue Investment Advisors

At Deep Blue Investment Advisors, we specialize in helping government finance officers expand their horizons by diving into fixed-income management solutions with tangible results. Our team of experienced investment management professionals can help tailor a portfolio to your investment needs while providing regular reporting, portfolio compliance, and performance meetings. You can always count on us to prioritize our relationships, provide guidance, and act in your best interest.

To speak with an advisor or for additional information about this article or Deep Blue Investment Advisors, please connect with one of our advisors today.

Deep Blue Investment Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. This communication is provided for informational purposes only and is not an offer to sell or a solicitation of an offer to buy any investments offered by Deep Blue Investment Advisors, nor shall any such investments be offered or sold to any person in any jurisdiction in which such an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Past performance is not an indicator of future results.

The information set forth herein is intended only for the person or entity to which it is addressed. By accepting this communication, you agree to maintain the confidentiality of its contents and agree not to distribute this communication to any other person or to use it other than for the purposes described above.