In a market where headline yields are hard to ignore, it’s easy to let a number make the decision for you. A higher rate on an unfamiliar product looks, at a glance, like a simple upgrade. But yield is only part of the story, and increasingly, it may be the part that leads you in the wrong direction. The real question isn’t “which fund pays the most?” It’s “does this vehicle match what I actually need to do with these funds?”

That distinction matters more right now than it has in years.

Not All LGIPs Are the Same, Even When They Look Like It

For a long time, shopping for a Local Government Investment Pool felt a lot like shopping for gas. The products were largely interchangeable, stable NAV or dollar-in-dollar-out, short duration, government-backed, and the only real differentiator was price. So investors looked at the yield, picked the highest one, and moved on. In that environment, that was a perfectly reasonable approach.

That environment no longer exists.

Today, not all LGIPs are stable NAV or dollar in dollar out. Some have credit risk. Some move like mutual funds. Others extend further out on the yield curve to capture higher returns, and they should, because they’re designed for a different purpose and a different holding period. The problem arises when an investor assumes a fund with a higher yield is simply a better version of what they already own. In many cases, it’s a different product entirely.

Even product names can be misleading. “Enhanced cash,” for example, means different things to different managers. For one firm, it might be a modest tilt away from overnight funds. For another, it might represent a meaningful shift in duration and NAV variability. The label alone is not enough information to make a sound decision.

Three Phases of the Rate Environment, and Where We Are Now

To understand why this is especially important today, it helps to look at how the rate environment has evolved.

Phase one was the post-COVID era of near-zero rates. With cash earning nothing, investors had to venture further out on the yield curve to generate any meaningful return. Duration carried risk, but it also carried reward. Some moved out deliberately; others may have chased yield without fully appreciating that they were taking on more time horizon than they realized.

Phase two was the Fed’s aggressive tightening cycle. Cash became king. Short-term, stable-NAV products suddenly outpaid longer-duration alternatives, an unusual inversion of the yield curve that made the simplest strategy the most profitable one. Yield shopping was not only acceptable, but it was also genuinely effective, because the products were truly interchangeable and short-end rates were the highest in the room.

Phase three is where we are now. Rates have been coming down through the cutting cycle. The inverted yield curve has started to normalize, meaning that longer-duration products are once again offering more than their overnight counterparts. That’s a return to a historically familiar relationship between time and yield, but it also reintroduces a trap that wasn’t a problem during phase two: chasing a higher rate can mean inadvertently extending your time horizon in ways that don’t match your actual needs.

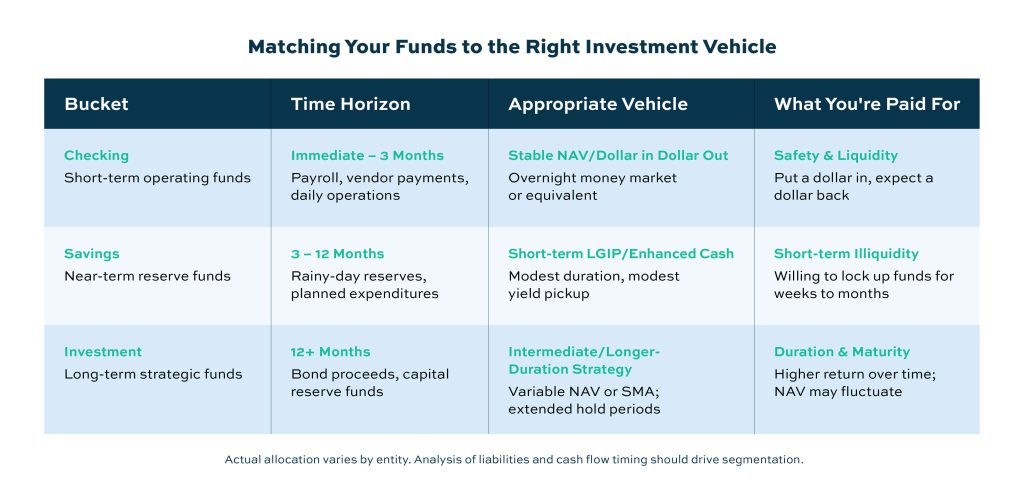

A Simple Framework: Checking, Savings, Investment

When helping a public entity think through how to allocate its funds, a useful starting point is the same mental model most of us use personally: checking account, savings account, and investment account.

- Checking account funds are due imminently or must be available on demand. Think payroll, vendor payments, and daily operations. These belong in a stable-NAV or dollar-in-dollar-out, overnight product. The goal here is not return, it’s certainty. Put a dollar in, expect a dollar back.

- Savings account funds aren’t needed tomorrow, but they’re not long-term either. Think three months to a year. These funds can tolerate a little more time commitment in exchange for a modestly higher yield, similar to a bank CD or high-yield savings product.

- Investment account funds are genuinely long-term, money that won’t be needed for many months or years. These can absorb NAV movement and benefit from the higher returns that come with extended duration, because time is on their side.

The allocation across these three buckets isn’t the same for every entity. One might need 70% in the short bucket, 20% in the middle, and 10% in the long. Another might look more like 85/10/5. What matters is doing the analysis honestly, looking at actual liabilities, budget commitments, and cash flow timing, and then matching your investment vehicles to that reality.

The Risk of Getting It Wrong Right Now

As interest income has declined alongside falling rates, some entities are feeling pressure to close the gap. It’s a natural response, budgets were built on higher projections, and there’s real institutional pressure to show yield performance. The temptation is to move toward longer-duration products to recover that income.

The problem is that those products are designed for a purpose. They’re built for funds that can sit for an extended period, weather NAV volatility, and ride out market noise. Overnight funds don’t belong there. And in a volatile environment, markets reacting to geopolitical uncertainty, shifting rate expectations, economic signals that aren’t moving in a straight line, an entity that moved short-term funds into a longer product for yield can find itself in a difficult position when it actually needs the money.

An entity with all of its funds in a stable overnight product barely feels that volatility. An entity that reached for yield is watching the tide come in and out. That distinction can go from a minor inconvenience to a genuine problem very quickly, depending on when liquidity is needed.

The One Rule Worth Carrying Into 2026

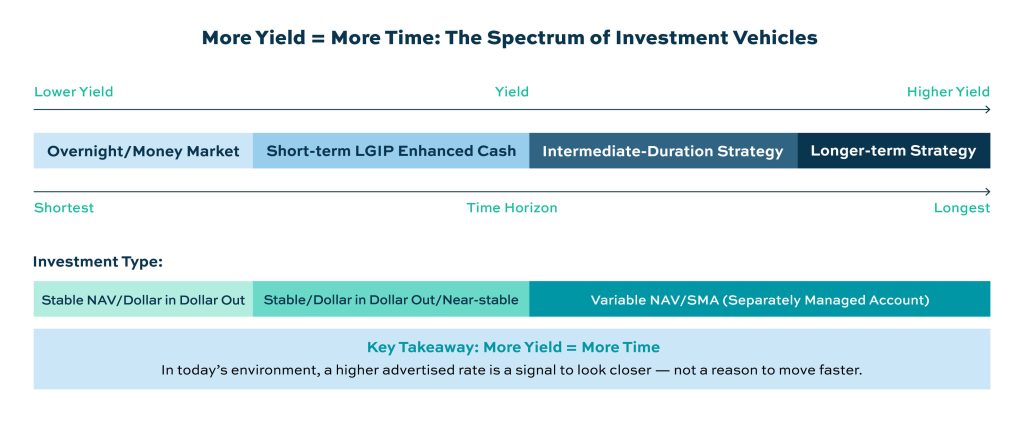

If there is a single heuristic that can help protect public entities from a yield-chasing mistake right now, it’s this: assume that more yield means more time.

In this environment, higher returns almost always come with a longer expected holding period, more NAV variability, or both. That isn’t a reason to avoid those products, it’s a reason to ask whether the funds you’re investing actually belong there. Start with yield as a signal. Don’t end there.

The homework required to answer that question, analyzing your liabilities, segmenting your cash, understanding the holding period of each dollar, is not glamorous. But it is what separates a well-structured portfolio from one that looks great on a rate sheet and creates headaches when the unexpected happens.

In 2026, it is a year where this homework matters. Not because the right answers are complicated, but because the cost of skipping it is higher than it has been in a while.

About Deep Blue Investment Advisors

At Deep Blue Investment Advisors, we specialize in helping government finance officers expand their horizons by diving into fixed-income management solutions with tangible results. Our team of experienced investment management professionals can help tailor a portfolio to your investment needs while providing regular reporting, portfolio compliance, and performance meetings. You can always count on us to prioritize our relationships, provide guidance, and act in your best interest.

To speak with an advisor or for additional information about this article or Deep Blue Investment Advisors, please connect with one of our advisors today.

*This article is for informational and educational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities or to adopt any investment strategy. Deep Blue Investment Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. Such registration does not imply a certain level of skill or training. The views expressed are those of the author as of the date of publication and are subject to change without notice. While information contained herein is believed to be reliable, Deep Blue Investment Advisors makes no representations or warranti