The fiscal year is an important planning tool, but may not always be the best proxy for investment horizon. Reviewing reserves and liquidity through the lens of actual cash needs may reveal whether public balances are still aligned with the portfolio built to serve them.

Public finance professionals operate in a world shaped by budgets, board calendars, audit cycles, legislative decisions, and year-end reporting. That structure is necessary. It drives planning, accountability, and governance. But it can also influence the way investment decisions are framed, sometimes more than the actual timing of cash needs.

When the fiscal year becomes the primary lens for evaluating reserves and operating balances, entities may default toward a shorter liquidity posture than their cash profile actually requires. Public funds demand caution, transparency, and flexibility. Still, the budget calendar and the true investment horizon of a public balance are not always the same thing.

Why the Fiscal Year Mindset Is So Common

This mindset is not the result of poor decision-making. In many cases, it reflects the practical realities of public funds management. Budgets are approved on a recurring cycle. Reporting is measured against fiscal periods. Oversight bodies often evaluate balances through the same lens. In that environment, defaulting to very short-term positioning can feel like the safer administrative choice.

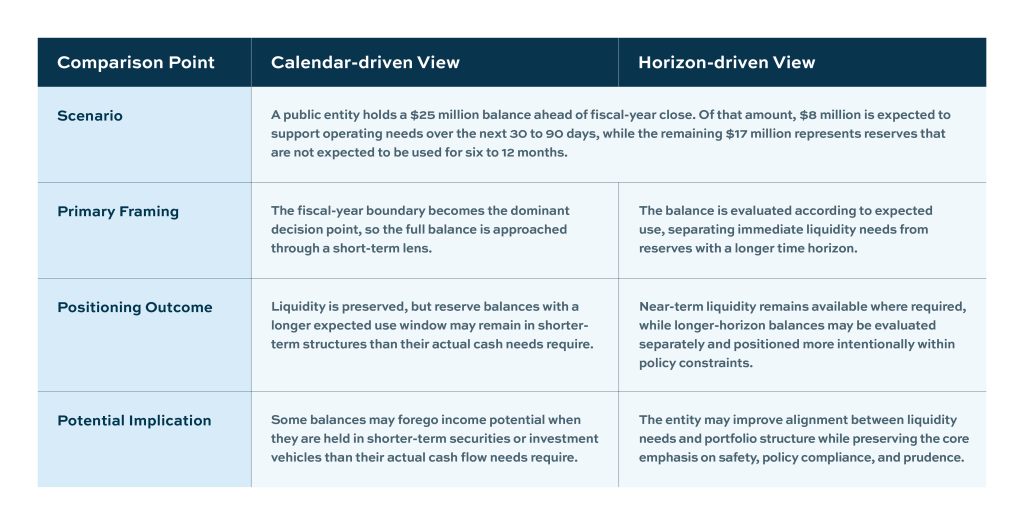

There is also a natural desire to preserve flexibility in case funds are needed sooner than expected. If a balance may be needed for operations, capital spending, or unexpected changes in revenue timing, shorter-term positioning can appear prudent. The challenge is that when this approach is applied equally to every dollar on the balance sheet, some balances may be positioned more conservatively than their actual liquidity needs require.

Why Other Considerations Matter

Public funds investing is ultimately guided by a familiar set of priorities: safety, liquidity, and return, subject to policy and statutory constraints. Framed that way, the next question becomes straightforward: when is the money actually needed?

Some balances truly should remain highly liquid. Operating cash, near-term disbursement needs, and uncertain flows generally belong there. But other balances may represent seasonal collections, project-related funds, or reserves that are not expected to be used immediately. When those balances are grouped into the same short-term mindset simply because they fall inside the same fiscal cycle, an entity may be foregoing income potential on balances whose actual liquidity needs are longer.

That distinction matters because liquidity is not the same as same-day liquidity. Public entities often need flexibility, but not every dollar requires the same degree of immediacy. A balance expected to support payroll next week should not be viewed the same way as a reserve that is unlikely to be touched for several months. Recognizing that spectrum can lead to a more precise and still-prudent approach to portfolio structure.

Illustrative Yield Comparison

Using the same $25 million example above, the difference can be framed in simplified annualized terms. This illustration is intended to show how a shorter average yield assumption and a longer average yield assumption may affect earnings potential.

A Better Framework: Segment by Purpose, Not Just by Calendar

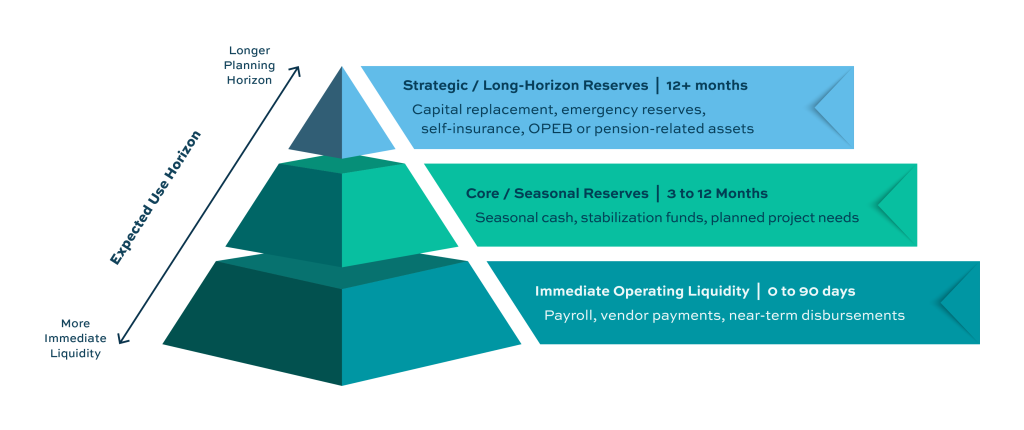

Rather than viewing all balances through the same budget-year lens, public entities may benefit from segmenting funds according to their actual role in the portfolio. In practice, that may mean separating immediate operating liquidity from intermediate balances with a more defined use window, and from strategic reserves that are not expected to be used in the near term.

In many cases, those longer-horizon balances may include stabilization reserves, capital replacement funds, utility renewal funds, self-insurance reserves, pension or OPEB prefunding assets, or emergency contingency funds. They do not all serve the same purpose, and they do not all require the same level of immediacy as day-to-day operating cash.

This framework is not about reaching for yield or stretching policy. It is about matching investments more intentionally to expected use while staying inside the entity’s own policy, statutory limits, and safety priorities. In practice, that can lead to a portfolio structure that better reflects how the entity actually operates rather than how the calendar is labeled.

Questions to Consider When Evaluating Public Balances

The Practical Takeaway

The fiscal year remains an important tool for planning and oversight. But it should not be the only framework for investing public funds. When the budget calendar becomes the default proxy for liquidity horizon, entities may overlook distinctions in purpose, timing, and expected use that matter to portfolio structure.

A more disciplined approach begins by identifying what each balance is for, when it is likely to be needed, and how much liquidity is truly required. From there, the portfolio can be structured with greater precision and with closer alignment between public balances and their intended role.

Each public balance serves a purpose. That purpose carries a time horizon. And that time horizon should help inform investment strategy. When funds are evaluated according to expected use rather than the fiscal calendar alone, governments may be better positioned to improve earnings, reinforce reserves, and steward public resources more effectively while remaining within established policy and risk parameters.

About Deep Blue Investment Advisors

At Deep Blue Investment Advisors, we specialize in helping government finance officers expand their horizons by diving into fixed-income management solutions with tangible results. Our team of experienced investment management professionals can help tailor a portfolio to your investment needs while providing regular reporting, portfolio compliance, and performance meetings. You can always count on us to prioritize our relationships, provide guidance, and act in your best interest.

To speak with an advisor or for additional information about this article or Deep Blue Investment Advisors, please connect with one of our advisors today.

Deep Blue Investment Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. This communication is provided for informational purposes only and is not an offer to sell or a solicitation of an offer to buy any investments offered by Deep Blue Investment Advisors, nor shall any such investments be offered or sold to any person in any jurisdiction in which such an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Past performance is not an indicator of future results.

The information set forth herein is intended only for the person or entity to which it is addressed. By accepting this communication, you agree to maintain the confidentiality of its contents and agree not to distribute this communication to any other person or to use it other than for the purposes described above.