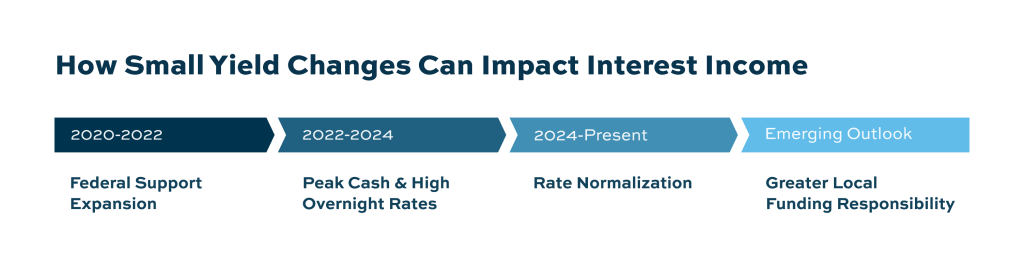

For many public entities, the last several years created an unusual environment. Federal funding expanded, liquidity was abundant, and strong short-term interest rates helped operating cash generate meaningful income with relatively little effort. Holding large balances in overnight structures often felt both safe and productive.

That environment may be starting to change.

As federal funding structures continue to evolve, municipalities, school districts, special districts, and other public entities may face a more constrained operating landscape over the next several years. Some programs may receive less federal support. Others may require greater local matching contributions or create additional pressure on already stretched operating budgets. The ultimate fiscal impact will vary by entity type and state, and the full picture is still taking shape, but the directional pressure is worth preparing for now.

The implications extend beyond budgeting.

They also raise important questions about reserve management, liquidity planning, and how public funds should be positioned in a less federally supported environment.

The End of “Easy Liquidity”

In periods of elevated federal support, cash balances often rise faster than expenditures. That creates flexibility. It also reduces pressure to optimize investment structures because liquidity itself feels abundant.

When that support begins to moderate or shift, the dynamic changes.

Entities may find themselves relying more heavily on reserve balances, local tax revenues, and internal cash flow management to support operations. At the same time, investment income may begin playing a larger role in helping offset budget pressure as federal support becomes less predictable.

In that environment, idle cash becomes more noticeable.

Funds that once sat comfortably in overnight accounts without much scrutiny may increasingly represent an opportunity cost worth reevaluating, especially as budgets tighten and operating expenses continue to rise. This does not mean public entities should abandon conservative investment principles. It means the definition of “productive liquidity” becomes more important.

A Different Kind of Budget Pressure

Most budget discussions focus on revenue and expenses. What often receives less attention is how investment strategy can either support or weaken financial flexibility during periods of transition.

If federal fiscal support declines while costs continue rising, many public entities will experience a familiar challenge: managing increasing obligations with constrained resources.

In prior years, elevated overnight rates helped offset some of that pressure. As rates normalize and funding structures evolve, simply holding excess cash in overnight vehicles may no longer provide the same benefit.

This creates a new layer of pressure:

- Expenses remain elevated

- Revenue growth may slow

- Federal fiscal support becomes less certain

- Interest income may decline at the same time

That combination makes cash management increasingly strategic rather than purely operational.

Why “Maximum Liquidity” Can Become an Expensive Habit

When uncertainty rises, many organizations default toward maximum liquidity. On the surface, that feels prudent. If funding timing is unclear or expenses may increase unexpectedly, keeping everything short and liquid appears safe.

The problem is that not all dollars share the same time horizon.

Operating cash needed for payroll, vendor obligations, or near-term projects should absolutely remain highly liquid. But reserve balances, stabilization funds, capital reserves, and longer-term allocations often have very different liquidity profiles.

Treating every dollar as immediately needed can quietly reduce portfolio effectiveness over time.

As rates decline, overnight products typically reset lower almost immediately, while longer-duration structures may continue benefiting from previously locked-in yields. At the same time, excess operating cash sitting entirely in overnight vehicles may earn materially less than funds positioned more intentionally across staggered maturities.

The result is not necessarily a liquidity problem. It is often an allocation problem.

Repositioning Does Not Mean Reaching for Yield

One of the biggest misconceptions in shifting environments is that improving returns requires taking significantly more risk.

For public entities, that is rarely the objective.

Repositioning is less about chasing higher returns and more about aligning investment structures with actual cash flow needs.

Of course, any repositioning strategy must remain aligned with state statutes, local investment policies, and the entity’s specific liquidity obligations.

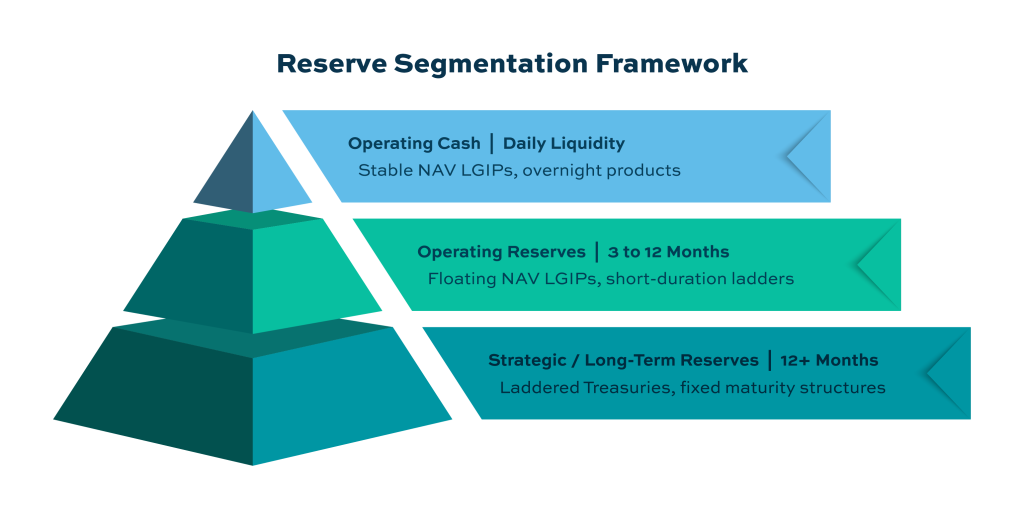

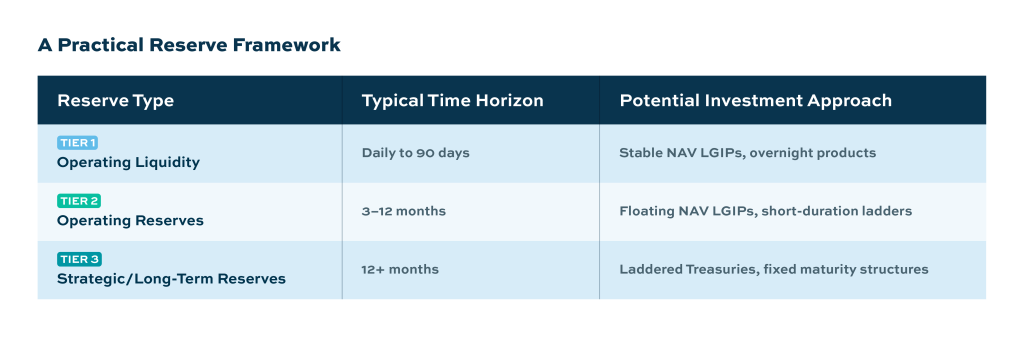

That process often begins with segmentation.

A Practical Reserve Framework

This framework helps distinguish between funds that truly require immediate access and funds that may reasonably tolerate a longer investment horizon.

For many entities, the exercise itself becomes valuable because it highlights how much liquidity is being maintained simply out of habit rather than necessity.

Consider a mid-sized school district with $30 million in reserves. On the surface, holding all of it in overnight accounts feels safe. But when leadership walks through the segmentation exercise, they may find that $8 million covers true operating needs, another $10 million serves as a stabilization cushion with a 6–12 month horizon, and the remaining $12 million is a capital reserve unlikely to be touched for two or more years. That final tranche, sitting in overnight cash, may be quietly costing the district meaningful income that could offset rising insurance premiums, deferred maintenance costs, or budget shortfalls without requiring a tax increase.

The Return of Laddering Strategies

The segmentation framework above naturally points toward laddering as a practical implementation strategy. As rate conditions evolve, laddering strategies are becoming more relevant again.

During periods of inverted yield curves and elevated overnight rates, staying entirely short often made sense. Today, that environment is beginning to normalize.

A laddered portfolio structure can help reduce dependence on any single rate environment while smoothing reinvestment risk over time. It also creates scheduled liquidity access points and may allow entities to capture incremental yield without taking on excessive duration exposure.

For example, instead of maintaining an entire reserve balance overnight, a municipality may stagger investments across:

- 3 months

- 6 months

- 9 months

- 12 months

As each maturity rolls off, funds become available for operations, reinvestment, or changing priorities.

The objective is not predicting rates perfectly. It is creating flexibility and consistency in a less predictable environment.

Investment Income May Matter More Than It Did Before

In strong revenue environments, investment income can feel secondary. In tighter conditions, it becomes more meaningful.

Even modest improvements in yield, when applied across large reserve balances, can generate meaningful contributions to the budget over time.

That additional income may not close a budget gap entirely, but it can help offset rising insurance costs, operational expenses, or deferred capital needs without increasing taxes or reducing services.

This is one reason why reserve positioning is increasingly becoming part of broader fiscal strategy discussions rather than remaining isolated within treasury operations.

Policy Reviews May Become More Important

As operating conditions evolve, many entities may also need to revisit their investment policies.

Not necessarily to increase risk tolerance, but to ensure policies reflect current realities.

Questions worth revisiting may include:

- Are reserve categories clearly defined?

- Does the policy distinguish between operating and strategic liquidity?

- Are maturity limits aligned with actual cash flow needs?

- Are approved investment vehicles broad enough to support flexibility?

- Is the entity unintentionally over-concentrated in overnight structures?

In many cases, policies written during lower-rate or different funding environments may not fully reflect today’s operational realities.

Thoughtful policy reviews can help ensure that investment strategy remains aligned with both liquidity needs and long-term financial objectives.

The Bigger Shift: Liquidity as a Strategic Asset

The broader takeaway from this environment is that liquidity is no longer just about accessibility.

It is becoming a strategic asset that requires active management.

For years, strong federal support and elevated short-term rates made simple cash management strategies effective. Public entities did not necessarily need to optimize every dollar because the environment itself was supportive.

That support may become less consistent moving forward.

As local governments absorb more responsibility for infrastructure, operations, and long-term financial stability, investment strategy may need to become more intentional alongside budgeting and forecasting efforts.

The entities that adapt well are unlikely to be the ones making dramatic portfolio shifts. More often, they will be the ones that clearly understand their liquidity needs, segment reserves intentionally, match investment horizons appropriately, and maintain flexibility without becoming overly concentrated in overnight cash positions. They will also be the ones willing to revisit policy assumptions as conditions evolve.

The next phase of public fund management may look less like maximizing liquidity at all times and more like balancing liquidity, income stability, and flexibility in a world where funding conditions are becoming more localized and less predictable.

In that environment, investment strategy becomes more than a compliance exercise. It becomes part of how long-term financial resilience is built.

About Deep Blue Investment Advisors

At Deep Blue Investment Advisors, we specialize in helping government finance officers expand their horizons by diving into fixed-income management solutions with tangible results. Our team of experienced investment management professionals can help tailor a portfolio to your investment needs while providing regular reporting, portfolio compliance, and performance meetings. You can always count on us to prioritize our relationships, provide guidance, and act in your best interest.

To speak with an advisor or for additional information about this article or Deep Blue Investment Advisors, please connect with one of our advisors today.

Deep Blue Investment Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. This communication is provided for informational purposes only and is not an offer to sell or a solicitation of an offer to buy any investments offered by Deep Blue Investment Advisors, nor shall any such investments be offered or sold to any person in any jurisdiction in which such an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Past performance is not an indicator of future results.

The information set forth herein is intended only for the person or entity to which it is addressed. By accepting this communication, you agree to maintain the confidentiality of its contents and agree not to distribute this communication to any other person or to use it other than for the purposes described above.